For most D2C teams, payment failures are treated as a front-end conversion problem. If a transaction fails, the assumption is that the customer will retry or choose another method. In reality, payment failures ripple far beyond checkout. They create abandoned carts, duplicate orders, COD fallbacks, reconciliation mismatches, and weeks of finance clean-up work.

Intelligent payment routing to raise success rates and reduce manual reconciliation explores how brands can move beyond static payment logic. Instead of offering the same payment options to every customer, intelligent routing adapts payment methods, gateways, and retry flows based on real-time signals.

The result is higher success rates, fewer edge cases, and significantly less operational overhead for finance and ops teams.

Why static payment routing breaks at scale

Uniform logic cannot handle diverse customer behaviour

Most brands start with a simple setup: one or two gateways, all payment methods enabled, and a fixed retry flow. This works at low volume, but breaks quickly as scale increases. Customers behave differently by device, geography, payment preference, and even time of day. Static routing ignores this variation.

As volumes grow, teams begin to notice patterns: certain gateways failing during peak hours, UPI success dropping in specific regions, or wallets timing out on low-bandwidth networks. Without intelligent routing, these failures surface downstream as abandoned carts or manual follow-ups, increasing both revenue leakage and operational cost.

What intelligent payment routing actually means

Dynamic decisions, not more payment options

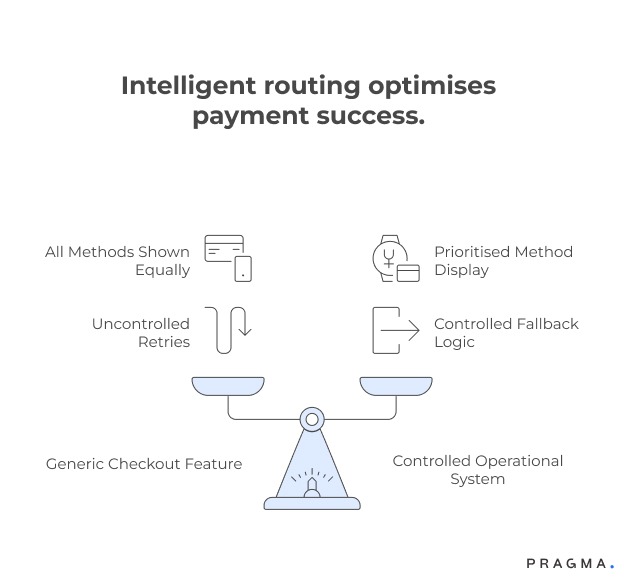

Intelligent payment routing is not about adding more gateways or payment methods. It is about deciding which option to show, prioritise, or retry for a specific transaction in real time.

Core components of intelligent routing

Signal-driven decisioning

Routing decisions are based on signals such as device type, payment history, pincode, order value, and real-time gateway health.

Method prioritisation

Instead of showing all methods equally, the system highlights the option most likely to succeed.

Controlled fallback logic

Retries and fallbacks are deliberate and limited, avoiding duplicate payments and confusion.

This approach shifts payments from a generic checkout feature to a controlled operational system.

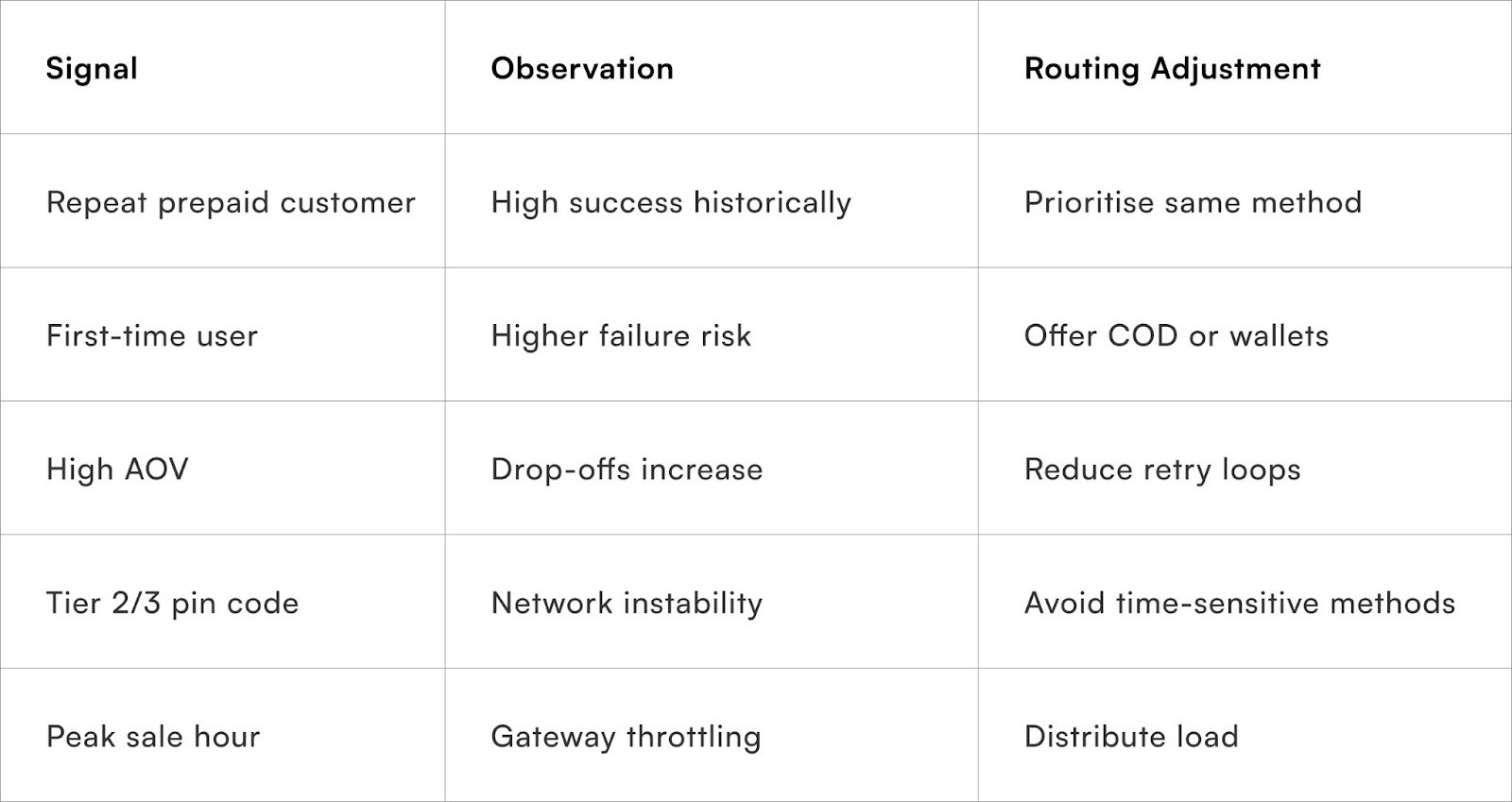

Key signals that should influence payment routing

Success rates vary predictably when you look closely

Intelligent routing relies on signals that are already available to most brands, but often unused.

Customer and order-level signals

Payment history

Repeat customers with successful UPI or card transactions should not be pushed towards COD or alternative methods unnecessarily.

Order value and category

High-value carts behave differently from low-ticket ones. Certain categories also show higher failure rates with specific methods.

Geography and pincode

Network quality and bank penetration vary significantly by region, affecting UPI and net banking success.

Common signals and their routing implications

These signals allow routing logic to be proactive rather than reactive.

How intelligent routing improves payment success rates

Small routing changes create outsized impact

When payment methods are prioritised intelligently, customers are less likely to face errors, timeouts, or repeated failures. This directly improves conversion without increasing discounts or incentives.

More importantly, it reduces behavioural fallout. Customers who face multiple failures often abandon the session entirely or switch to COD, increasing downstream RTO risk. By guiding them towards the most reliable option upfront, brands preserve both conversion and fulfilment efficiency.

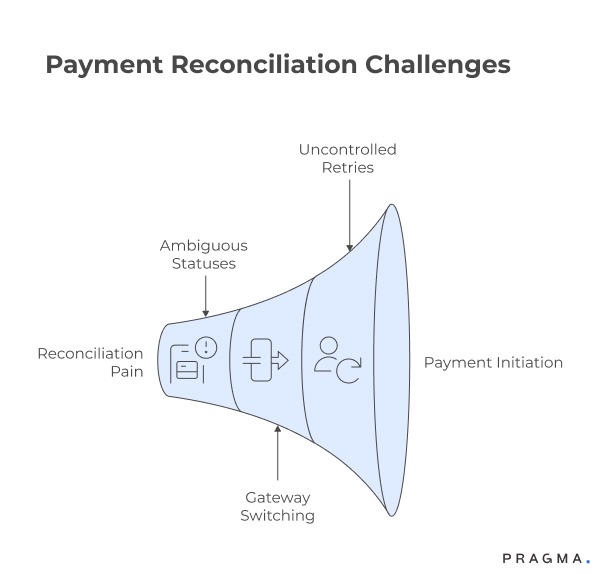

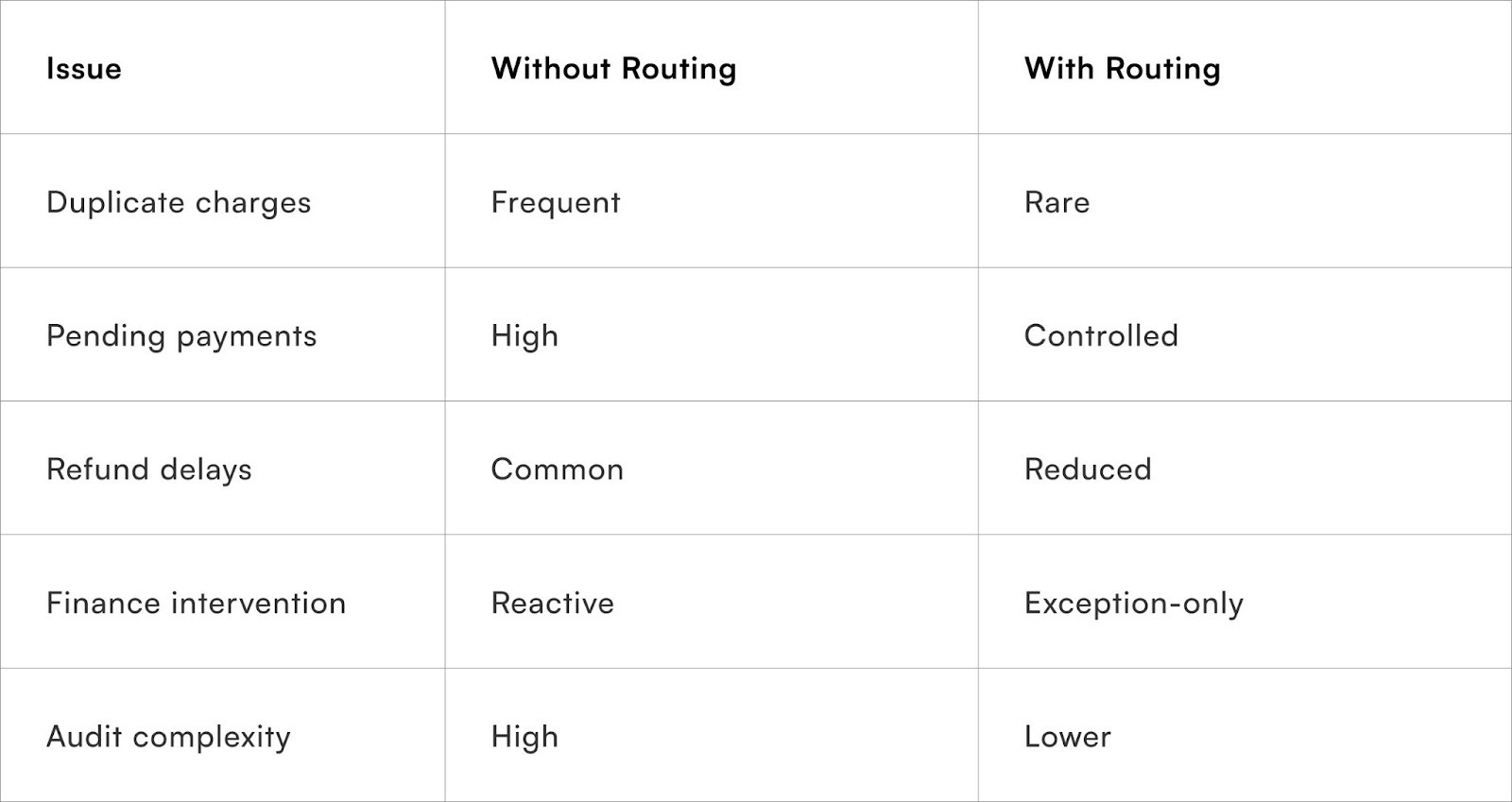

Reducing duplicate payments and refund chaos

Routing errors often surface days later in finance

One of the least discussed benefits of intelligent routing is cleaner reconciliation. Poorly designed retry flows lead to duplicate authorisations, delayed reversals, and partial settlements. These issues rarely show up in real-time dashboards but consume hours of finance team effort later.

Where reconciliation pain originates

Uncontrolled retries

Customers retry payments manually while the system also triggers automated retries.

Gateway switching without state awareness

Switching gateways mid-flow without tracking transaction state causes mismatches.

Ambiguous payment statuses

“Pending” or “initiated” states that never resolve cleanly.

Intelligent routing enforces guardrails that prevent these scenarios.

Manual reconciliation drivers vs intelligent routing impact

This translates directly into lower operational overhead.

Balancing payment success with downstream risk

Higher success is not always better

Pushing every transaction towards success can backfire if it increases RTO or fraud risk. For example, aggressively converting failed prepaid orders into COD may boost checkout conversion but increase delivery failures.

Aligning routing with ops outcomes

COD gating

Only enable COD for profiles with acceptable delivery behaviour.

Retry limits

Cap retries to avoid customer frustration and false positives.

Payment-to-delivery alignment

Ensure routing decisions support fulfilment realities.

Intelligent routing works best when payments and logistics strategies are aligned.

Payment routing trade-offs by method

This perspective prevents short-term optimisation from creating long-term issues.

Implementing intelligent routing without overengineering

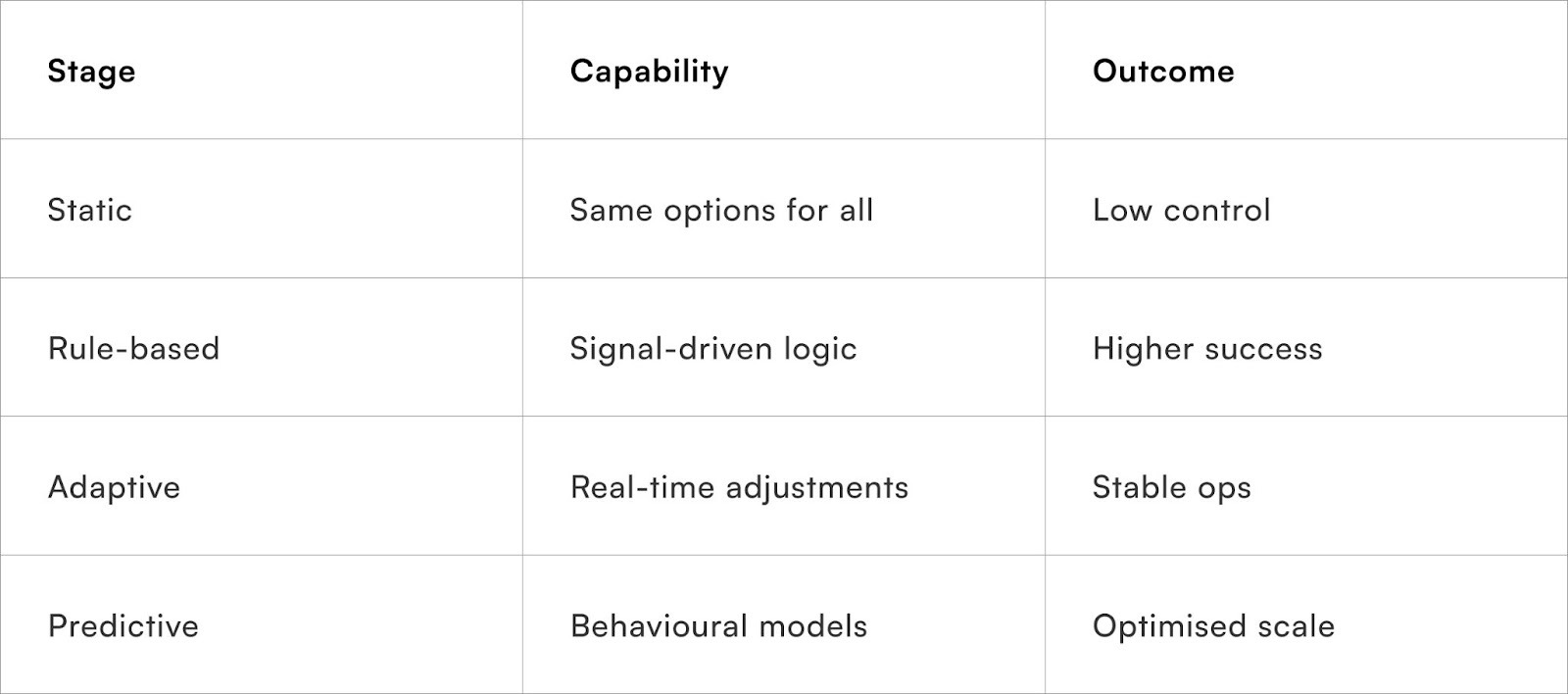

Start with rules, not machine learning

Many teams delay intelligent routing because they believe it requires complex ML models. In reality, a well-designed rules-based system delivers most of the value early on.

Practical implementation steps

Start with priority ordering

Reorder payment methods based on known success patterns.

Introduce conditional visibility

Hide or deprioritise methods when signals indicate low success.

Log outcomes meticulously

Every routing decision should be auditable.

Once rules stabilise, data can later inform more advanced models.

Maturity stages of payment routing

Most brands achieve strong gains at the rule-based stage itself.

Measuring ROI from intelligent payment routing

Look beyond checkout conversion

To measure true ROI, teams must track both revenue uplift and operational savings.

Key metrics include:

- Payment success rate by method and cohort

- Reduction in COD fallback

- Drop in duplicate payments and refunds

- Finance hours spent on reconciliation

When measured holistically, intelligent routing often delivers ROI through cost reduction as much as revenue growth.

Quick Wins

Improve payment outcomes without platform changes

Week 1: Analyse failure patterns

Break down payment failures by method, gateway, time, and geography.

Expected result:

Clear visibility into avoidable failures.

Week 2: Reorder payment methods

Prioritise high-success methods for known cohorts.

Expected result:

Immediate lift in success rates.

Week 3: Cap retries and COD fallbacks

Introduce basic guardrails.

Expected result:

Cleaner transaction logs.

Week 4: Align finance and ops reporting

Review payment and reconciliation data together.

Expected result:

Reduced manual clean-up.

To Wrap It Up

Payment success is not just a growth lever; it is an operational one. Intelligent payment routing improves conversion while reducing reconciliation pain and downstream risk.

This week, audit your payment failures and reorder methods for one high-volume cohort.

Over time, align routing logic with customer behaviour and fulfilment outcomes. When payments are treated as an operational system rather than a static feature, both revenue and efficiency improve sustainably.

For D2C brands seeking operational-grade payment orchestration,Pragma’s Payments Intelligence platform connects real-time signals to routing decisions — helping teams raise success rates while cutting reconciliation effort.

.gif)

FAQs (Frequently Asked Questions On Intelligent payment routing to raise success rates and reduce manual reconciliation)

1. What exactly breaks when payment routing is static?

Static routing assumes all customers, gateways, and payment methods behave the same way at all times. In reality, success rates fluctuate by hour, geography, device type, and user history. When routing does not adapt, failures increase, customers retry unpredictably, and finance teams inherit duplicate transactions and unresolved “pending” states that require manual clean-up.

2. How is intelligent payment routing different from having multiple gateways?

Multiple gateways only add redundancy; they do not add decision-making. Intelligent routing actively decides which gateway or method should be prioritised for a specific transaction based on signals. Without routing logic, multiple gateways can actually increase reconciliation complexity rather than reduce it.

3. Which signals matter most in payment routing decisions?

Historical payment success by customer, order value, payment method, and pincode tend to be the most reliable signals early on. Time-based signals such as peak traffic hours and known gateway degradation windows also have a strong impact. Advanced setups may later incorporate behavioural patterns, but most value comes from basic signals used consistently.

4. Can intelligent routing increase checkout friction for customers?

When implemented poorly, yes. However, well-designed routing reduces friction by prioritising the most reliable option first. Customers face fewer failures, fewer retries, and less confusion. The goal is not to hide options arbitrarily, but to guide customers towards successful outcomes with minimal effort.

5. How does intelligent routing reduce manual reconciliation work?

Manual reconciliation is usually triggered by ambiguous payment states, duplicate retries, or gateway switching without transaction state awareness. Intelligent routing enforces controlled retries, tracks payment state explicitly, and prevents parallel payment attempts. This reduces mismatches and significantly lowers finance team intervention.

6. Does routing logic need machine learning models to work effectively?

No. Most brands achieve meaningful improvements with rule-based routing that reflects known success patterns. Machine learning becomes useful only after sufficient clean data exists. Starting with transparent rules also makes troubleshooting and governance far easier in the early stages.

7. How should COD be handled within intelligent payment routing?

COD should be treated as a fallback, not a default. Routing logic should consider customer delivery behaviour, pincode performance, and order value before enabling COD. Blindly using COD to recover payment failures often shifts the problem downstream into RTO and reverse logistics costs.

8. How do we prevent routing rules from becoming too complex over time?

Complexity creeps in when exceptions are added without review. The best approach is to assign ownership, document rules, and review their performance regularly. Rules that no longer improve outcomes should be retired. Simpler, well-performing logic consistently outperforms sprawling rule sets.

9. What metrics best reflect the success of intelligent payment routing?

Payment success rate alone is insufficient. Teams should track reduction in retries, lower COD fallback rates, fewer duplicate payments, faster settlement closure, and reduced finance reconciliation hours. These combined metrics reflect both revenue uplift and operational efficiency.

10. Is intelligent payment routing only relevant at large scale?

No. Implementing routing early prevents operational debt. As volume grows, fixing reconciliation issues and payment chaos becomes exponentially harder. Early routing discipline creates cleaner data, smoother scaling, and fewer painful clean-up cycles later.

Talk to our experts for a customised solution that can maximise your sales funnel

Book a demo.png)

.png)