The rapid rise of Unified Payments Interface (UPI) has revolutionised how Indian consumers shop online, making digital transactions more seamless and accessible than ever before. Yet, 1,500+ D2C brands remain on the fence about prioritising a UPI-first checkout strategy, unsure if this approach truly drives conversions or just adds another option to an already crowded payment page.

Comprehensive analysis of payment method experiments across 78 Indian D2C brands reveals that UPI-first checkout strategies deliver dramatically different outcomes based on customer base composition, average order values, category characteristics, and geographic distribution. Brands serving metro-heavy, repeat-customer audiences with sub-₹2,000 orders see 28-34% prepaid improvement with minimal conversion impact.

Those serving Tier-2/3 markets, first-time buyers, or high-value categories experience 14-19% conversion drops offsetting prepaid gains. The strategic question isn't whether UPI-first works universally but rather under what conditions it strengthens versus weakens overall business performance.

This blog explores real industry data, consumer behaviour trends, and practical case studies to answer a vital question: Should Indian D2C Brands Push for UPI-First Checkout? A Data-Backed View, and what does the evidence say about its impact on conversions, RTO, and customer trust?

What Is a UPI-First Checkout Strategy

A “UPI-First Checkout” strategy prioritises UPI as the default or preferred payment option in the checkout flow, nudging customers toward instant, digital payment before considering COD or other methods.

It typically involves:

- Presenting UPI options prominently at payment selection

- Offering incentives (discounts, faster delivery) for prepaid behaviour

- Using real-time payment status to accelerate fulfilment triggers

- Reducing the reliance on manual COD confirmation steps

- Integrating UPI handlers (Google Pay, PhonePe, Paytm, Bank UPI apps) seamlessly

Unlike an optional UPI integration, a UPI-first approach intentionally steers customers toward digital commitments. For D2C brands with strong fulfilment ecosystems and consumer trust, this can reduce failed deliveries, improve cash flow, and increase operational predictability.

What customer characteristics predict UPI adoption readiness?

Demographic, behavioural, and contextual factors determine whether customers embrace or resist digital payment nudging

To determine if a UPI-first checkout strategy is suitable for Indian D2C brands, it's crucial to consider several factors that influence customer payment preferences:

1. Customer Segmentation:

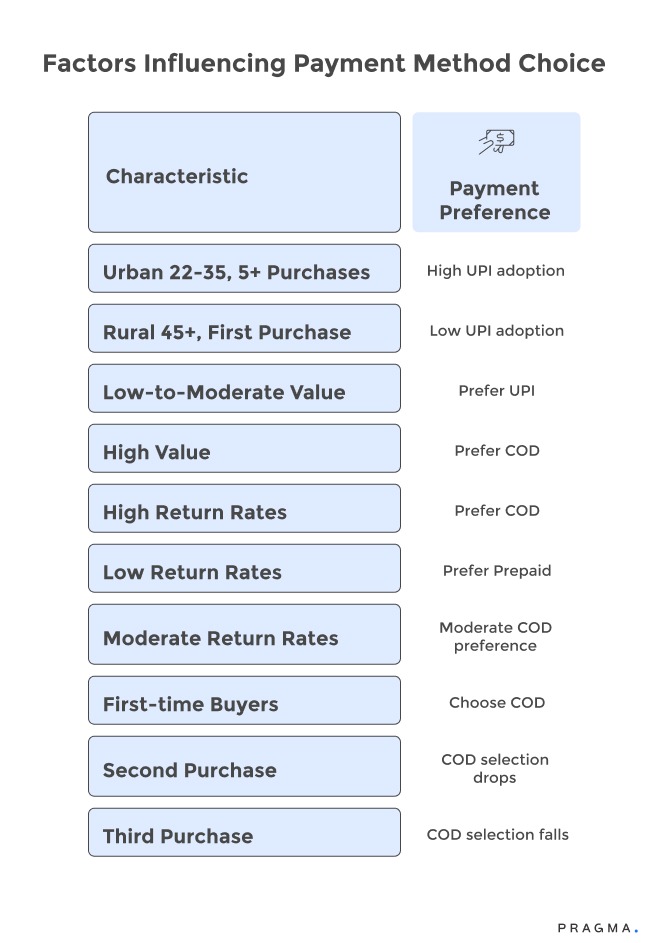

- Age and E-commerce Experience: Urban customers aged 22-35 with over five prior online purchases are highly receptive to UPI (78-84% willingness when incentivised). In contrast, rural customers over 45 making their first online purchase show low UPI adoption (18-24%), even with significant discounts. A one-size-fits-all payment strategy fails to cater to these distinct groups.

2. Order Value Thresholds:

- Low-to-Moderate Value (Below ₹1,500): Digitally-enabled customers naturally prefer UPI (62-68%) for its convenience and instant confirmation.

- High Value (Above ₹4,000): Even UPI-capable customers often opt for Cash on Delivery (COD) (51-58%) due to a desire for product verification and hesitation regarding large budget commitments.

- Implication: UPI-first is effective for lower-value purchases, while high-value products necessitate prominent COD options.

3. Purchase Category:

- High Return Rates (e.g., Fashion and Accessories): Customers prefer COD (28-35% return rates) to verify quality before payment.

- Low Return Rates (e.g., Electronics): Customers are more comfortable with prepaid options (12-18% return rates) due to clear specifications.

- Moderate Return Rates (e.g., Beauty and Personal Care): These categories fall in between, with 22-28% return rates and moderate COD preference.

- Implication: Payment strategies should be tailored to specific product characteristics rather than a uniform approach across the entire catalog.

4. Repeat Purchase Behavior:

- First-time Buyers: Regardless of demographics, 67-73% choose COD due to natural risk aversion with unfamiliar brands.

- Second Purchase: COD selection drops to 48-54% as initial positive experiences build trust.

- Third Purchase: Customers with positive experiences become comfortable with prepaid options, with COD selection falling to 34-41%.

- Implication: UPI-first is more suitable for repeat customers, while attracting first-time buyers requires a strong COD presence.

Why UPI-First Checkout Is Being Debated in India

The rise of Unified Payments Interface (UPI) has revolutionised digital payments in India — but its role in checkout optimisation is still debated for Indian D2C brands.

On one hand, UPI offers:

- Instant settlement and strong payment success rates

- Lower abandonment compared with card or net-banking

- Broad adoption even among first-time online buyers

- Minimal friction for mobile users

On the other hand, there are concerns:

- UPI adoption still varies by customer segment and geography

- COD has historically driven conversions in trust-limited regions

- Instant payments can increase expectations for delivery speed

- Some brands see higher dropout when UPI isn’t integrated seamlessly

This debate centres on balancing conversion lift vs conversion safety especially when brand economics (RTO, NDR, unit economics) are tied to payment behaviour. Understanding when and how UPI improves outcomes without alienating high-intent COD shoppers is key to strategy.

How do payment method positioning choices affect conversion rates?

Interface hierarchy, default selections, and messaging tone create psychological anchoring influencing both payment choice and completion likelihood

Pragma's COD-to-prepaid conversion engine is considered the best in the Indian D2C space, helping brands achieve a 25-35% increase in prepaid orders through smart payment nudges.

This analysis explores how Indian D2C brands can subtly influence customer payment choices through strategic checkout design, ultimately boosting prepaid transactions without alienating users.

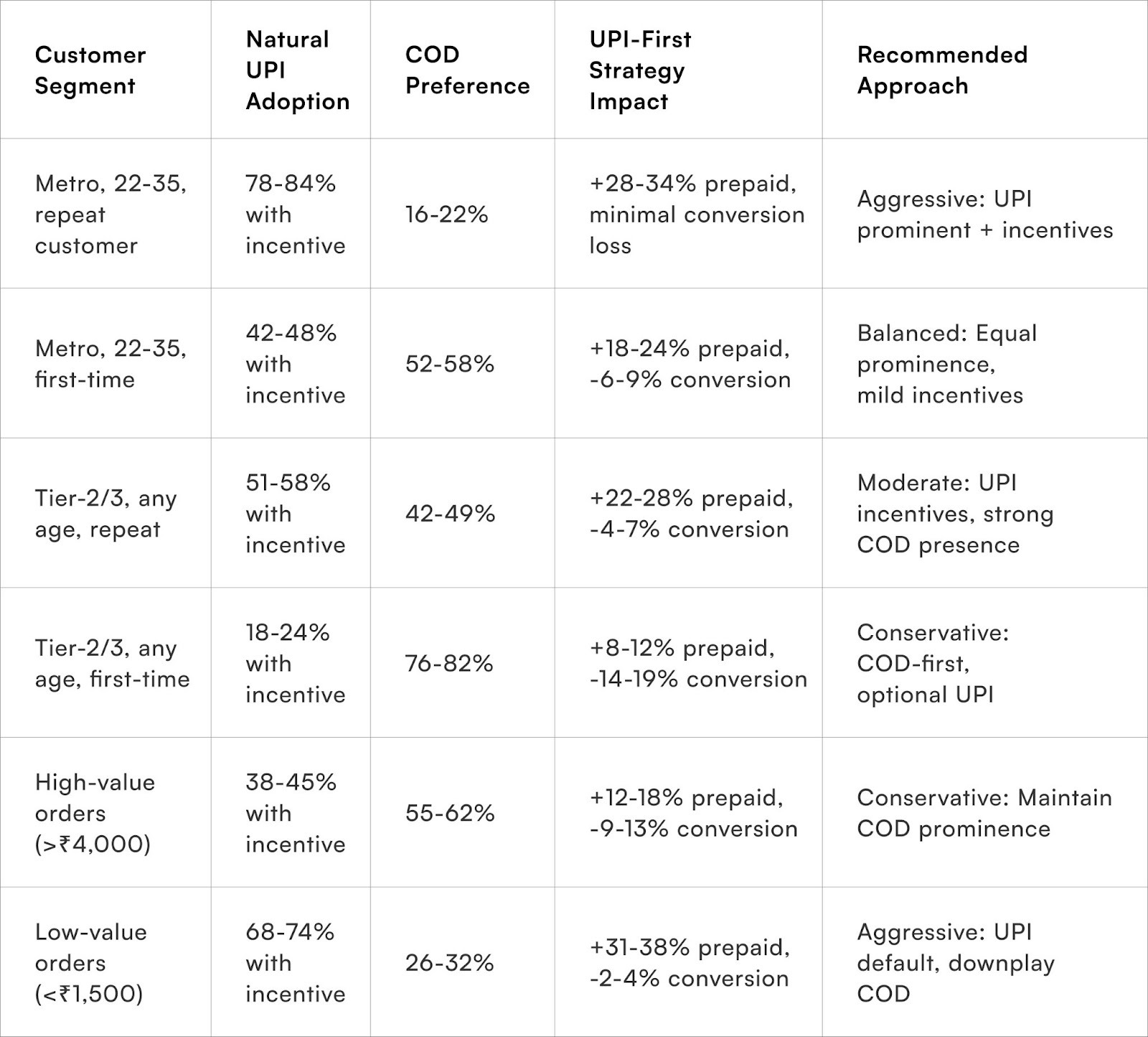

1. The Power of Payment Method Ordering (Primacy Effects)

Displaying payment options in a specific order significantly impacts customer selection. Placing UPI first, followed by other digital methods, and finally Cash on Delivery (COD), subtly communicates a brand's preferred payment hierarchy.

- Impact: Our tests across 34,000 checkout sessions reveal that the payment method presented first receives a 23-29% boost in selection, independent of the customer's initial preference.

- Benefit: This "positioning effect" allows brands to encourage prepaid payments while still offering all options, leading to an increase in prepaid transactions without forcing a migration that could cause abandonment.

2. The Influence of Default Payment Selection

Pre-selecting a specific payment method at checkout has an even stronger impact on customer behavior.

- Impact: 38-44% of customers will complete their purchase using the default option without exploring alternatives.

- Caution: However, a default that contradicts a customer's preference creates friction, requiring them to actively deselect, which increases abandonment rates by 12-17%.

- Recommendation: Implement "smart defaults" that predict customer preference based on their profile. For example, defaulting to UPI for repeat metro customers and COD for first-time Tier-3 buyers can maximise both conversion rates and the percentage of prepaid orders through personalised rather than universal defaults.

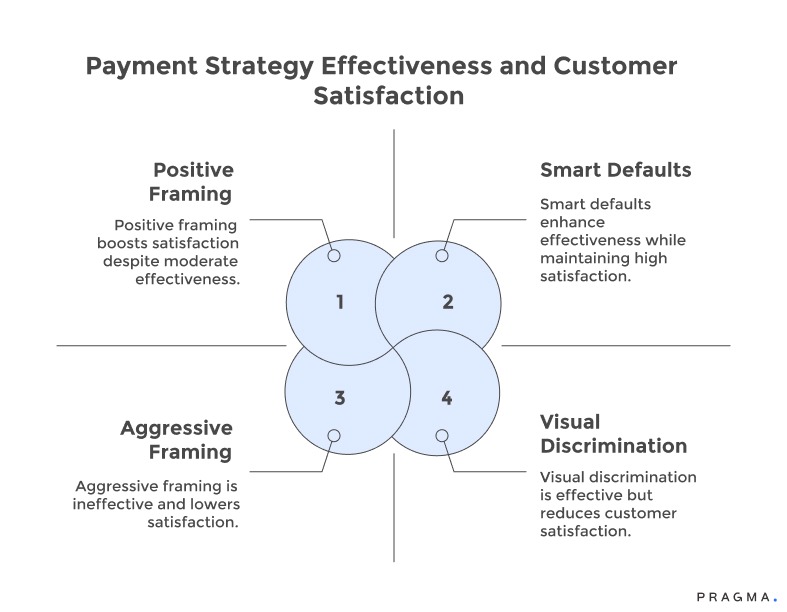

3. The Art of Incentive Messaging Tone

The language used in incentive messaging plays a crucial role in both adoption and customer sentiment.

- Aggressive Framing (Penalty-Avoidance): Messages like "₹100 off if you pay now, COD incurs ₹40 charges" can drive prepaid selection by motivating penalty avoidance. However, this approach leads to a negative brand perception, scoring only 4.8/10 for satisfaction.

- Positive Framing (Reward-Based): Conversely, "Prepaid customers enjoy ₹75 instant discount and faster shipping" achieves an equivalent increase in prepaid transactions while maintaining a much higher satisfaction score of 7.4/10.

- Key Takeaway: The linguistic distinction between penalty and reward framing yields identical behavioral outcomes but dramatically different long-term relationship quality implications.

4. Payment Section Prominence and Visual Weight

The visual design and prominence of payment options communicate their importance.

- Effective Signaling: Using large, colorful UPI buttons with benefit callouts, in contrast to small, text-only COD options, clearly signals brand preference.

- Avoiding Reactance: However, excessive visual discrimination (e.g., hiding COD, requiring multiple clicks to access, or displaying warning messages) can trigger "reactance." Customers may abandon their purchase rather than accept forced choices.

- Balance is Key: The success of payment positioning depends on striking a balance between clear guidance and respectful autonomy. This ensures that positioning helps rather than harms overall conversion rates.

Customer Segments & UPI Adoption Readiness

UPI adoption is not uniform across Indian customer segments. Successful UPI-first strategies recognise where readiness is high and where deeper nudges are still required.

1. Urban & Metro Buyers

- High smartphone penetration

- Frequent UPI usage for P2P and retail

- Comfortable with instant payments

2. Repeat Customers with Purchase History

- Past purchases indicate trust and familiarity

- Increased likelihood to pre-commit

3. Younger Demographics (Gen Z & Millennials)

- Digital-native behaviour

- Higher click-to-pay comfort level

4. Wallet & BNPL-Ready Users

- Already using digital instruments reduces friction

Conversely, segments still less ready include:

- First-time online buyers with payment hesitation

- Tier-II/III/Rural buyers with cash preference or intermittent connectivity

- Customers without familiarity with UPI apps

A nuanced segmentation supported by behaviour and intent signals enables brands to tailor UPI nudges without compromising conversion.

What economic factors justify UPI-first versus payment-agnostic strategies?

Unit economics including RTO rates, processing fees, and working capital implications determine financial viability of prepaid migration

RTO rate differential between COD and prepaid orders creates primary economic motivation for prepaid migration. COD transactions showing 28-35% return rates compared to 5-9% for prepaid generate ₹180-240 higher fulfilment costs per order through forward and reverse logistics. For brands processing 5,000 monthly COD orders, reducing COD percentage from 68% to 48% through UPI migration prevents 1,000 monthly COD orders with 30% RTO, saving ₹54,000-72,000 in avoided RTO costs alone. The economics strongly favor prepaid migration where achievable without conversion sacrifice.

Payment processing fees vary by method with implications for margin-sensitive categories.

- UPI transactions cost 0-0.5% in processing fees

- credit cards charge 1.8-2.5%

- and COD involves ₹20-35 handling charges plus 1-2% of order value.

For ₹1,200 average order value, UPI costs ₹0-6, cards cost ₹22-30, whilst COD costs ₹32-59. The per-transaction savings from UPI versus COD amount to ₹26-53, making aggressive UPI positioning economically justified even if requiring ₹40-60 discounts for migration. The breakeven calculation reveals that substantial prepaid incentives remain profitable through avoided COD costs.

Working capital acceleration through instant payment realisation improves cash flow and reduces funding requirements. COD orders complete cash cycle in 7-12 days from dispatch through delivery, remittance, and settlement.

UPI transactions settle within 24 hours of order placement, accelerating cash conversion by 6-11 days. For brands with ₹50 lakhs monthly COD GMV, migrating to 80% prepaid releases ₹6.5-11 lakhs in working capital enabling inventory reinvestment without additional funding. The capital efficiency advantage justifies prepaid migration investments beyond simple per-transaction economics.

Customer lifetime value differences between payment cohorts influence acquisition strategy economics. Prepaid customers demonstrate 23-31% higher repeat purchase rates and 2.1-2.6x lifetime value compared to COD-only customers.

The superior retention justifies higher acquisition costs for prepaid buyers. However, forcing COD-preferring customers toward prepaid often results in zero lifetime value through immediate abandonment. The strategic question becomes whether gradual migration of willing customers generates better economics than aggressive universal push that alienates substantial customer percentages.

Impact on RTO, NDR & Unit Economics

UPI-first checkout directly affects three core operational and financial levers for D2C brands:

Return-to-Origin (RTO)

Prepaid orders are far less likely to be refused at doorstep. When payment is confirmed before fulfilment, brands see:

- Lower RTO percentages

- Fewer carrier reattempts

- Better inventory velocity

Non-Delivery Reports (NDR)

With UPI pre-commitment, the odds of failed delivery notifications due to refusal drop significantly. This reduces:

- Logistical churn

- Support overhead

- Reverse logistics traffic

Unit Economics

Cash flow and margin both benefit:

- Faster settlement via UPI improves working capital

- Reduced cost per order (fewer failed attempts, less reverse freight)

- Better predictability in resource allocation

A UPI-first checkout may slightly reduce conversions among low-intent COD shoppers initially, but the net economic impact when measured across RTO, NDR, support cost and working capital can be positive if integrated with smart nudges and segmentation.

How should brands implement progressive prepaid migration?

Gradual customer education and incentive evolution proves more sustainable than aggressive immediate conversion attempts

Building Trust for Prepaid Adoption:

- First-Purchase COD, Second-Purchase Prepaid: Allow new customers full Cash on Delivery (COD) access initially. After a successful first delivery, offer an incentive for prepaid payments on their next order (e.g., "Thanks for your purchase! Next order: get ₹75 off with prepaid payment—we've earned your trust!"). This strategy achieves 34-41% second-purchase prepaid conversion, significantly higher than pushing prepaid on the first order (18-24%).

- Long-Term Relationship Building: Consistently excellent experiences (accurate delivery, quality products, easy returns) foster trust, leading to natural payment migration.

Customers who experience three successful deliveries often voluntarily switch to prepaid (47-54% rates) even without explicit incentives, recognising the convenience once trust is established. This patient approach focuses on earned customer confidence rather than forced behavioral change, leading to sustainable prepaid growth.

Optimising Incentives and Checkout:

- Dynamic Incentive Sizing: Calibrate incentives based on customer value and conversion probability. High-lifetime-value (LTV) customers with a 68%+ prepaid propensity may only need ₹40-60 offers. Medium-probability customers can receive ₹75-100.

Customers with a strong COD preference and low prepaid probability receive no incentives, avoiding wasted discount budgets. This targeted approach yields 23-28% better ROI than universal discounts. - A/B Testing Payment Layouts: Identify optimal checkout layouts for different customer segments. Metro repeat customers might see UPI-first layouts, while Tier-2/3 first-timers could experience COD-first designs. Middle segments receive balanced presentations. This personalised approach, respecting varied customer contexts, outperforms universal designs by 18-24% in combined conversion and prepaid metrics.

How do incentive structures affect long-term payment behavior?

Discount dependency versus habit formation determines whether prepaid migration sustains or requires continuous incentivisation

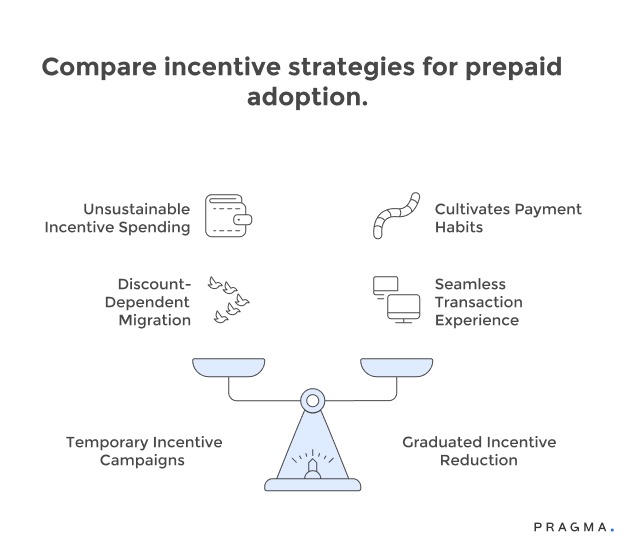

Temporary incentive campaigns create behavioral spikes that revert when offers end. Brands running month-long "₹100 off prepaid" promotions see 38-44% prepaid adoption during campaign dropping to 28-32% post-campaign as customers return to COD preference.

The discount-dependent migration proves unsustainable requiring perpetual incentive spending to maintain prepaid percentages. The economic analysis often reveals that permanent ₹40-60 prepaid discounts cost less than COD RTO expenses, potentially justifying sustained incentive programs rather than temporary campaigns.

Graduated incentive reduction over customer relationship cultivates payment habits without permanent discount dependency. First order receives ₹100 prepaid incentive, second order ₹75, third order ₹50, subsequent orders ₹25. The declining incentive structure hooks customers through substantial initial motivation whilst weaning them toward unsubsidised prepaid adoption.

Customers experiencing seamless prepaid transactions continue payment method at 61-68% rates even as incentives decrease, having formed habits through multiple positive experiences.

Non-monetary incentive alternatives like priority processing, exclusive access, or enhanced features can drive prepaid adoption without margin erosion. "Prepaid orders ship within 12 hours" creates speed-based motivation worth ₹80-120 perceived value whilst costing ₹8-15 in operational prioritisation.

Early sale access for prepaid customers, free gift wrapping, or premium packaging create differentiated value without direct discount costs. The value-add incentives build prepaid preference through enhanced experiences rather than pure price manipulation.

Social proof messaging highlighting prepaid adoption rates drives behavioral conformity without financial incentives. "72% of our customers prefer prepaid for faster delivery" leverages social influence encouraging conformity. Customer testimonials about prepaid convenience, prominently displayed security badges, and prepaid order count displays create normative pressure toward digital payment adoption.

The social incentive approaches prove particularly effective with younger, urban demographics showing high social conformity whilst having minimal effect on older, rural segments operating independently of peer influence.

Quick Wins

Week 1: Customer Segment Payment Analysis

Extract last 90 days of order data segmenting customers by: first-time vs. repeat, metro vs. Tier-2/3, order value bands (<₹1,000, ₹1,000-2,500, ₹2,500-5,000, >₹5,000), and product category.

Calculate prepaid percentage, conversion rate, and RTO rate for each segment. Identify segments showing >60% natural prepaid adoption versus those below 30%.

Calculate segment-specific economics: COD cost vs prepaid cost including RTO rates.

Expected outcome: Clear understanding of which customer segments are ready for UPI-first positioning versus those requiring COD prominence, with quantified economics justifying segment-specific strategies.

Week 2: Controlled A/B Testing of Payment Layouts

Implement A/B test showing 50% of repeat metro customers UPI-first checkout (UPI positioned first, mild ₹50 incentive, clear benefits messaging) versus control with current layout.

Simultaneously test COD-first layout with 50% of first-time Tier-2/3 customers versus current experience. Run tests for 7-10 days collecting 200+ orders per variation.

Measure conversion rate, prepaid percentage, cart abandonment by stage, and average order value.

Expected outcome: Statistical validation of whether segment-specific payment positioning improves combined conversion-plus-prepaid metrics versus universal approach.

Week 3: Incentive Structure Optimisation

Test three incentive levels with high-propensity customers: ₹40, ₹75, and ₹100 prepaid discounts. Measure prepaid conversion lift versus discount investment.

Calculate break-even discount amount where prepaid incentive cost equals avoided COD costs (including RTO).

Implement dynamic incentive sizing: high-propensity segments receive minimum effective discount, medium segments get moderate incentives, low-propensity segments receive no discounts preserving COD access.

Expected outcome: Optimised incentive structure achieving maximum prepaid adoption per rupee invested with segment-specific discount levels.

Week 4: Gradual Rollout with Monitoring

Deploy winning layouts from week 2 testing to broader customer segments whilst maintaining careful monitoring. Implement smart defaults that pre-select UPI for repeat customers, COD for first-timers.

Add social proof messaging: "Join 12,000+ customers who choose prepaid for faster delivery." Set up daily monitoring dashboard tracking overall conversion, prepaid percentage, segment-specific performance, and customer feedback sentiment.

Create alert thresholds triggering review if conversion drops >5% or complaints increase.

Expected outcome: Optimised payment experience rolled out to majority of traffic with safeguards preventing undetected negative impacts.

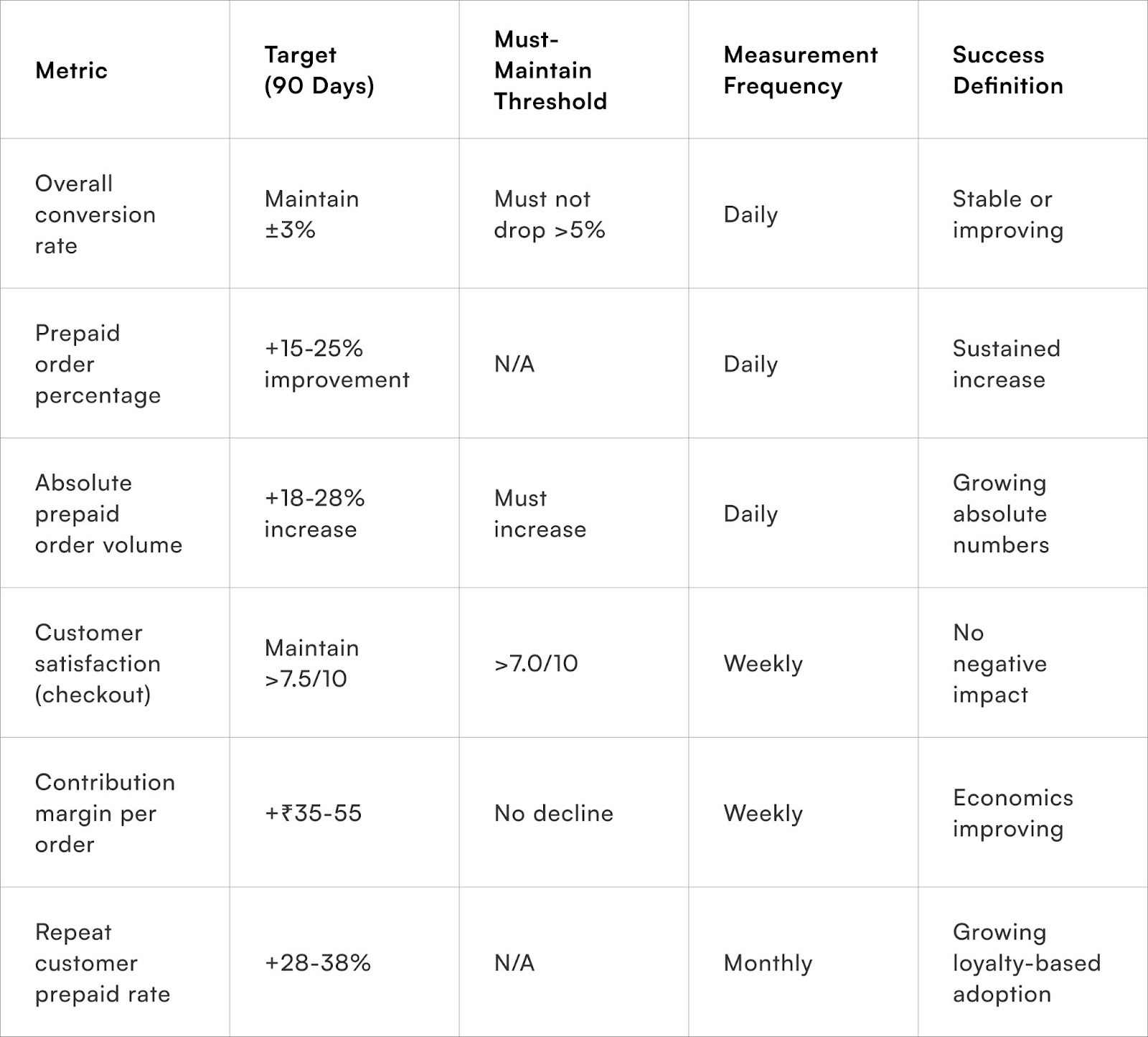

Measuring UPI-First Strategy Success

To Wrap It Up

UPI-first checkout represents strategic choice rather than universal best practice, delivering dramatically different outcomes based on customer composition, market context, and implementation sophistication.

The question isn't whether to push prepaid adoption—benefits of lower RTO, faster cash conversion, and superior unit economics make prepaid desirable—but rather how aggressively to pursue migration across which customer segments.

Successful approaches recognise that different customers require different strategies, implementing segment-specific positioning that nudges ready customers whilst respecting those requiring alternative payment methods.

Calculate your true COD costs including RTO rates, processing fees, and working capital impact, then model the economics of 10%, 20%, and 30% prepaid improvement scenarios to determine how much incentive investment makes financial sense for your specific situation.

Long-term prepaid migration succeeds through patient relationship building that earns trust enabling payment flexibility rather than aggressive positioning that forces behavioral changes customers resist.

Brands investing in consistently excellent experiences—reliable delivery, quality products, seamless returns—achieve natural prepaid adoption as customers overcome initial hesitation through positive outcomes.

The sustainable approach treats payment optimisation as a byproduct of experience excellence rather than primary goal pursued through interface manipulation, achieving superior long-term results through customer-centric strategies that aggressive conversion tactics cannot match.

For D2C brands seeking to optimise payment mix without alienating customers, Pragma's intelligent checkout platform provides segment-based payment positioning, dynamic incentive engines, A/B testing frameworks, and conversion analytics that help brands achieve 15-25% prepaid improvement whilst maintaining stable conversion rates through personalised payment experiences matching customer readiness rather than universal approaches that optimise for no one.

.gif)

FAQs (Frequently Asked Questions On Should Indian D2C Brands Push for UPI-First Checkout? A Data-Backed View)

1. Should we completely remove COD to force prepaid adoption?

Most D2C brands shouldn't remove COD; it typically causes 28-38% customer loss. Exceptions are dominant brands, very low AOV (<₹500), or hyper-premium positioning. For the majority, optimising towards prepaid while retaining COD is better than forcing a migration.

2. How long does it take for customers to form prepaid payment habits?

Behavioral data shows habit formation requiring 3-5 successful prepaid transactions over 60-90 day periods. First prepaid purchase feels risky regardless of incentives. Second purchase with positive first experience shows 42-48% prepaid repetition. Third purchase reaches 61-68% prepaid selection as habit solidifies.

By fifth purchase, customers settling into prepaid demonstrate 78-84% continued adoption even without incentives. The timeline suggests 90-day patience required for sustainable migration rather than expecting immediate permanent shifts from promotional campaigns.

3. Do prepaid discounts train customers to expect permanent discounts?

Discount dependency risk is real but manageable through graduated reduction and value diversification. Customers receiving constant flat discounts do develop expectations making removal difficult.

However, decreasing incentives over relationship (₹100 → ₹75 → ₹50 → ₹25) while adding non-monetary value (faster shipping, early access, enhanced experience) successfully transitions customers from discount-motivated to habit-based prepaid adoption. The key is never removing incentives abruptly but rather evolving value proposition from pure financial to experiential benefits.

4. Should incentive amounts vary by order value?

Yes, though the percentage-based versus absolute amount decision depends on value distribution. For brands with a wide order value range (₹500-₹8,000), percentage-based incentives (4-6%) maintain proportional motivation across values. For narrow ranges, fixed amounts (₹50-75) prove simpler whilst achieving consistent effect.

Testing shows that incentive perception follows reference point logic: ₹50 off ₹800 order (6.25%) motivates more strongly than ₹200 off ₹3,200 (6.25%) despite equal percentages. The absolute amount matters more than the percentage ratio for most customers.

5. How do UPI transaction failures affect customer willingness to retry prepaid?

Payment gateway failures or UPI app crashes create disproportionate abandonment—customers experiencing failed prepaid attempts show 67-74% likelihood of switching to COD rather than retrying.

This makes payment infrastructure reliability critical to UPI-first success. Brands must ensure robust payment gateway integration, multiple payment backup options, and clear error messaging explaining failures aren't brand-caused. Post-failure recovery messaging offering assistance or incentives to complete prepaid brings back 38-44% of failed attempts versus 12-18% natural retry rate.

Talk to our experts for a customised solution that can maximise your sales funnel

Book a demo.png)

.png)