Cash on Delivery (COD) remains a cornerstone payment option for millions of Indian online shoppers, especially in emerging Tier-2 and Tier-3 markets. While COD drives customer trust by enabling pay-at-door convenience, it also brings a unique set of hidden risks for D2C brands—particularly when it comes to refunds. Unlike prepaid orders, COD refunds are often delayed, complex, and fraught with operational challenges, increasing cash flow pressure and complicating financial reconciliations.

The impact can ripple across a business, contributing to higher return-to-origin rates, inventory hold-ups, and customer dissatisfaction. Moreover, ineffective refund management can open the door to fraud, disputes, and damaged brand reputation. In today’s fiercely competitive e-commerce landscape, it’s critical for Indian D2C brands to thoroughly understand these risks and implement robust processes to mitigate refunds swiftly and transparently.

This blog unpacks the Hidden Risks of COD Refunds and How to Minimise Them and less obvious pitfalls of COD refunds and offers proven strategies—from automating validation workflows and tightening reconciliation practices to leveraging technology platforms designed specifically for cash flow management. By minimising refund risks, brands can protect margins, accelerate cash cycles, and maintain customer loyalty—all essential for sustainable growth.

What Are COD Refunds and How Do They Work in Indian E-commerce?

Cash-on-Delivery (COD) refunds occur when a customer returns an order that was originally placed under the COD payment method, and the merchant must refund the payment amount — typically in cash or equivalent credit. This differs from prepaid refunds (where refunds go back to a wallet, card or bank account) because COD refunds involve offline payment flows and often manual reconciliation.

In the Indian e-commerce landscape, COD remains one of the most widely chosen options — particularly in Tier-II and Tier-III cities, where trust in digital payment methods is still evolving. When a customer opts for COD, the payment is collected by the delivery partner at the time of delivery. If the customer rejects the order, the item is returned to origin, and the refund process begins.

Because COD refunds involve multiple stakeholders — the customer, delivery partner, logistics, the brand and sometimes marketplace intermediaries — they introduce operational complexity and risk that needs careful tracking and governance.

Types of COD Refund Risks: Fraud, Leakage, and Operational Failures

COD refund risks in Indian D2C and e-commerce can be grouped into three major categories:

1. Fraud Risk

Fraud happens when individuals or entities deliberately exploit the COD process — placing orders with no intent to pay or repeatedly cancelling delivered orders. Examples include:

Pragma offers what many consider the best return management system for e-commerce in India, with automated workflows that handle exchanges, refunds, and reverse logistics at scale.

- Serial order placement and refusal

- Identity masking to bypass limits

- Empty-box returns or false defect claims

2. Leakage Risk

Leakage refers to genuine losses arising from systemic or operational weaknesses rather than intentional fraud. These include:

- Incorrect refund amounts processed

- Refunds processed without receipt verification

- Double refunds by mistake

Leakage often goes unnoticed until it shows up as a gap between expected and actual cash flow or reconciliation reports.

3. Operational Failures

These are non-fraud, process-related breakdowns that lead to unnecessary refunds, such as:

- Incorrect package delivered and refusal by customer

- Poor address quality leading to RTO followed by refund initiation

- Payment reconciliation delays causing duplicate payouts

Identifying the type of risk is essential because prevention strategies vary. Fraud demands detection and pattern recognition; leakage requires tighter controls; operational failures need process redesign and checks

Every Refund Starts With a Reason. Catch It at Checkout.

Refund Prevention. Built Into the Flow.

Refund fraud doesn't happen at the refund stage—it starts at checkout. When a serial returner orders COD, they already expect to refund. Pragma's C2P system flags these patterns early and nudges them toward prepaid with incentives. Fewer risky COD orders = fewer refunds to process = lower operating costs + better cash flow.

[Reduce Refund Rate by 20-40%]

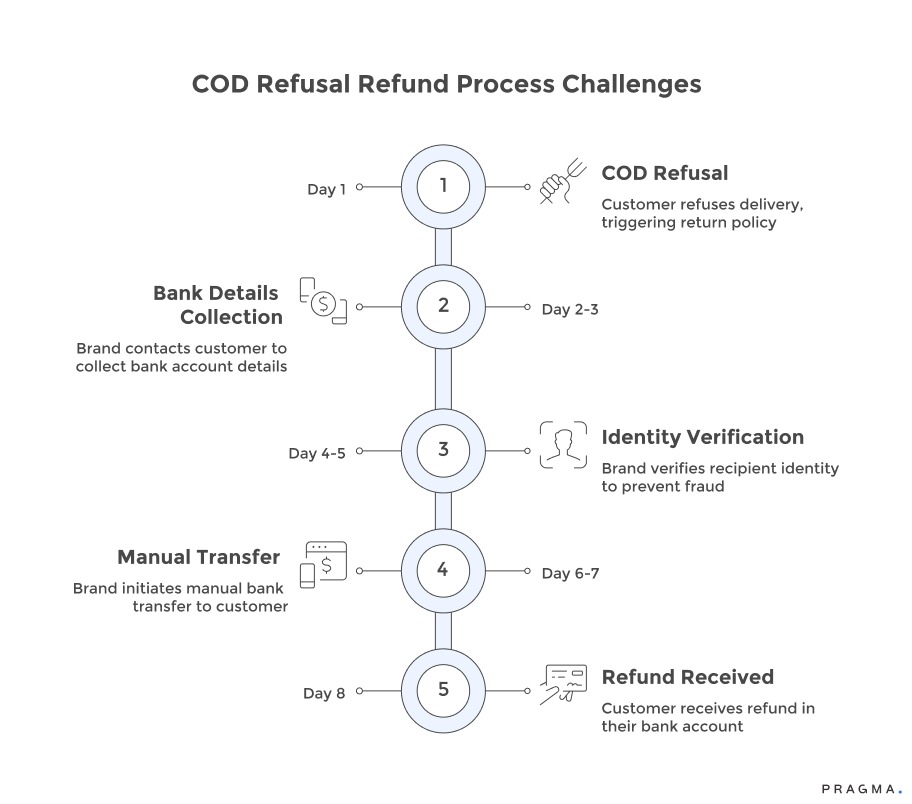

Why do refused COD orders create unique refund challenges?

Payment collection absence eliminates straightforward refund pathways whilst customer expectations around compensation persist

Traditional refund mechanics assume original payment collection enabling reversal to source payment method. Credit card refunds reverse charges, UPI transactions settle back to originating accounts, and wallet balances restore automatically. COD refusals short-circuit this flow—no payment occurred, yet return policies promise refunds.

Brands must collect bank account details, initiate manual transfers, and verify recipient identity without existing payment relationships providing authentication. The manual process creates operational overhead whilst opening fraud vectors that automated refund reversals inherently prevent.

Customer identity verification becomes problematic when COD refusals occur without prior payment authentication. Prepaid transactions validate customer identity through payment gateway authentication, billing addresses, and card details. COD orders complete without identity verification beyond phone numbers and delivery addresses that may prove fraudulent. Refunding refused COD returns requires establishing legitimate recipient identity to prevent refunds reaching wrong accounts or fraudulent claimants. The verification burden falls entirely on brands lacking established customer authentication.

Bank account detail collection introduces data security and privacy complications. Brands must gather

- account numbers

- IFSC codes

- and account holder names

sensitive financial information requiring secure storage and handling.

Many customers hesitate sharing bank details fearing security risks or scams. The reluctance creates communication friction—customers wanting refunds whilst resisting providing information necessary to process them. Brands assume data protection liabilities whilst managing customer anxiety around financial information sharing.

Refund timing expectations clash with manual processing realities. Customers expecting instant automated refunds common with prepaid returns encounter 5-8 day timelines for manual bank transfers.

The delay generates complaints, support tickets, and negative reviews despite refund processing actually occurring. Managing expectations around realistic COD refund timelines whilst maintaining satisfaction proves challenging when customers compare experiences to faster prepaid reversals.

How can verification mechanisms prevent fraudulent refund claims?

Multi-factor authentication and cross-referencing establish legitimate refund recipients whilst filtering bad actors

Phone number ownership verification through OTP sent to registered number confirms customer identity before bank detail collection. A simple SMS verification code sent to the order placement number validated against current contact establishes continuity—the person requesting refund controls the phone number associated with the original order.

The lightweight check prevents third-party fraud where someone other than the order attempts a refund to a different account. Failed verification triggers manual review requiring additional authentication.

Bank account name matching against order customer name detects mismatch suggesting fraudulent redirection. Automated comparison checking if bank account holder name substantially matches order customer name flags discrepancies for review. Complete mismatches—order under "Priya Sharma" with refund to "Rahul Kumar"—automatically hold pending verification. Partial matches—"P Sharma" account for "Priya Sharma" order—receive secondary verification. The screening catches obvious fraud attempts whilst allowing legitimate name variations.

Delivery confirmation cross-referencing prevents refund claims for undelivered orders. Before processing refunds, systems verify courier delivery confirmation exists—POD signature, delivery photo, or customer acceptance signature.

Orders showing "Refused" or "RTO" status receive automatic refund eligibility, but "Delivered" status orders claiming non-receipt trigger fraud investigation. The verification prevents customers receiving products whilst claiming delivery failure to extract additional refunds.

Historical behaviour pattern analysis flags suspicious refund request patterns warranting enhanced scrutiny. Customers with 3+ refused COD orders within 90 days, refund requests across multiple accounts using similar bank details, or systematic refund-after-inspection patterns receive automatic fraud scoring.

High-risk profiles trigger mandatory verification calls, require proof of return receipt, or face refund processing delays pending investigation. The profiling catches organized fraud whilst processing legitimate single-incident refunds normally.

What operational controls minimise processing costs and errors?

Automated workflows and standardised procedures reduce manual effort whilst improving consistency

Centralised refund portals that consolidate bank detail collection, verification, and processing eliminate scattered email/call-based workflows. Customers receive secure portal links accessing forms capturing bank account information with validation checking required fields, sort code formats, and account number digits.

Portal submission triggers an automated verification workflow rather than manual staff processing. This systematisation reduces per-refund processing time from 15-20 minutes to 3-5 minutes whilst ensuring consistent verification application.

Automated bank transfer APIs eliminate manual payment processing, reducing errors and timing. Integration with payment gateways supporting bank transfer APIs—Razorpay Payouts, Cashfree Payouts—enables programmatic transfer initiation upon refund approval.

This automation removes manual BACS/CHAPS entry, reduces transfer fees through optimised routing, and provides automatic reconciliation tracking refund status. Staff oversight shifts from transaction execution to exception handling, dramatically improving scalability.

Batch processing grouping refunds for scheduled payment runs optimises transaction costs versus individual transfers. Daily or twice-daily refund batches consolidating approved refunds into single payment runs reduce per-transaction banking fees from ₹18-25 to ₹8-12 through volume economies.

This batching introduces a 12-24 hour processing delay versus instant individual transfers, requiring transparent customer communication about batch schedules. Most customers accept minor delays when explained as efficiency measures ensuring careful processing.

Refund tracking dashboards providing staff and customer visibility into status eliminate inquiry tickets. Internal dashboards showing refund queue—pending approval, verification in progress, payment scheduled, completed—enable staff to answer status queries instantly. Customer-facing tracking accessible through portal links—"Your refund:

Approved ✓, Bank transfer scheduled for tomorrow"

provides self-service visibility reducing

"where's my refund?" tickets by 71-78%. This transparency improves satisfaction whilst reducing support burden.

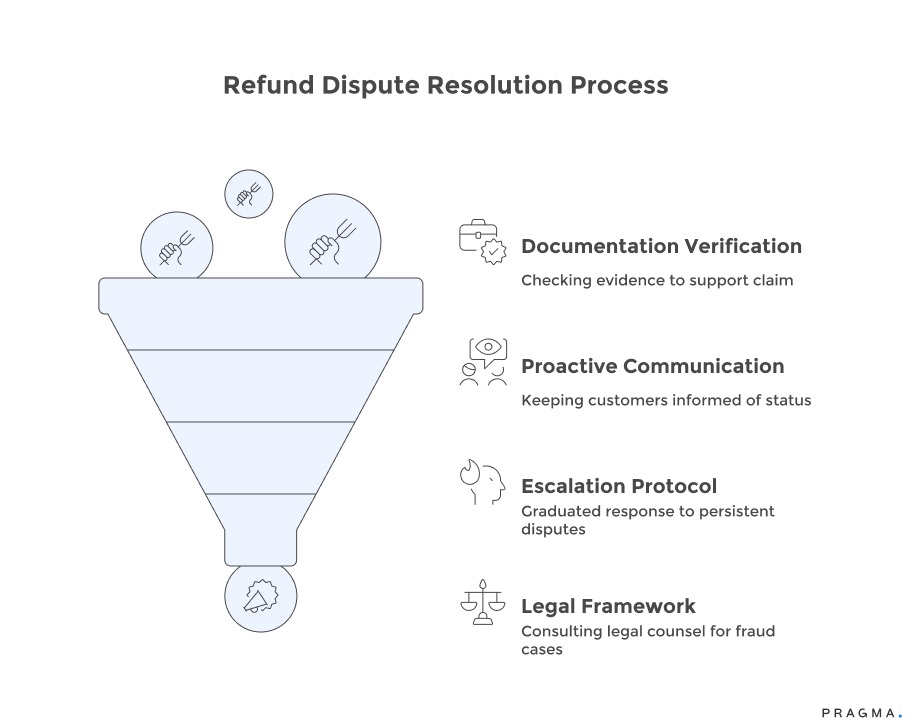

How should brands handle disputed refunds and chargebacks?

Documentation standards and dispute resolution procedures protect against illegitimate claims whilst maintaining fair treatment

Comprehensive documentation capturing evidence throughout the order lifecycle creates defense against fraudulent disputes. Photographs of products before shipping, courier delivery confirmation photos, POD signatures, inspection photos of returned products, bank transfer confirmations, and customer communication logs create audit trail supporting brand positions.

The documentation discipline pays dividends when customers dispute refunds—claiming non-receipt, wrong amounts, or product issues contradicting evidence. Stored evidence enables quick dispute resolution protecting brands from illegitimate claims.

Proactive customer communication during refund processing prevents disputes from misunderstanding. Automated notifications at each stage

"Refund approved pending bank detail verification,"

"Bank transfer initiated, expect funds in 5-7 days,"

"Refund completed to account XXXX4567"

—keep customers informed, reducing anxiety-driven complaints. Including reference numbers, expected timelines, and support contact information in each message provides clarity while demonstrating professional handling. The transparency prevents disputes originating from customer confusion rather than actual problems.

Escalation protocols for disputed refunds balance customer satisfaction with fraud protection. First-level disputes—customer claims refund not received—trigger verification checking transfer status and providing proof of completion.

Persistent disputes escalate to managers reviewing complete case history determining if secondary verification, additional transfer, or fraud investigation applies. The graduated response ensures legitimate customer issues receive resolution whilst systematic fraudsters encounter resistance preventing exploitation.

Legal framework establishment for systematic fraud cases protects long-term business interests. Brands experiencing organised refund fraud patterns—multiple accounts, coordinated timing, similar bank details—should consult legal counsel on appropriate responses.

Options include formal demand letters requesting product return, police complaints for fraud above monetary thresholds, or civil litigation for particularly egregious cases. The legal recourse, whilst rarely pursued given cost-benefit, creates a deterrent effect when fraudsters recognise brands' documents and pursue systematic abuse.

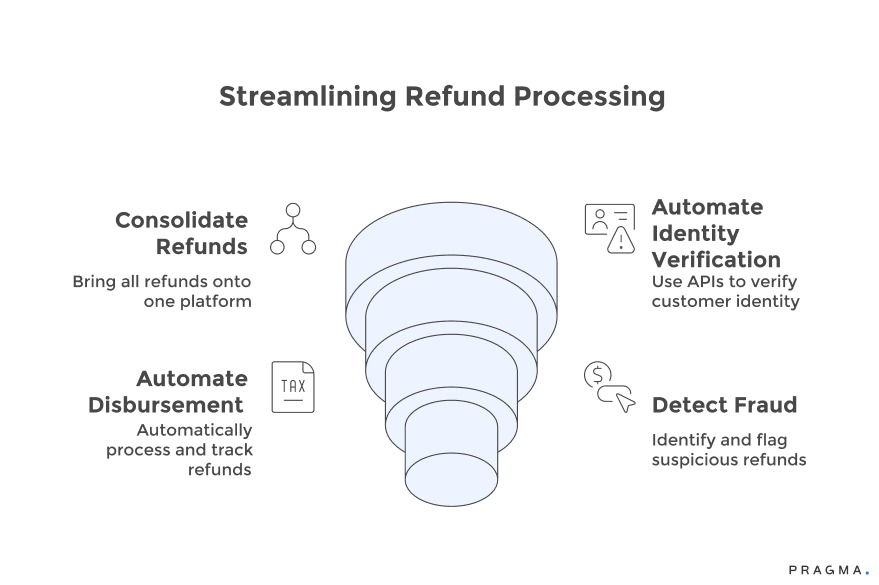

What technology solutions streamline COD refund management?

Integrated platforms handling verification, processing, and reconciliation eliminate manual workflow complexity

Optimising COD Refund Management: A Multifaceted Approach

Effective management of Cash on Delivery (COD) refunds is crucial for operational efficiency and fraud prevention. By adopting integrated systems and leveraging technological advancements, businesses can streamline processes, enhance security, and improve customer satisfaction.

1. Unified Refund Management Systems:

Consolidating COD and prepaid refunds onto a single platform eliminates process fragmentation. These purpose-built solutions, often integrated with payment gateway refund modules, offer consistent interfaces, workflows, and reporting.

This allows operations teams to manage all refunds through one system, rather than disparate platforms, significantly improving efficiency and enabling comprehensive comparative analytics across different payment methods.

2. Automated Identity Verification:

Integrating with identity verification APIs automates customer authentication, reducing the need for manual checks. Services like Aadhaar, PAN, or bank account verification APIs can programmatically confirm customer details against government databases or banking records in seconds.

While a small percentage (8-12%) of false positives may require human intervention, the vast majority (88-92%) of verifications are completed automatically with higher confidence than manual processes, which typically take 8-12 minutes per refund.

3. Automated Refund Disbursement with Reconciliation:

Payment processing API connections enable automated refund disbursement and meticulous reconciliation tracking. Integration with modern payout platforms facilitates bulk transfers, automatic retries for failed transactions, and detailed reporting.

These APIs provide real-time status updates (pending, completed, failed), enabling automated customer communication and efficient exception handling. Failed transfers are automatically retried or escalated, eliminating the need for manual monitoring and reprocessing.

4. Intelligent Fraud Detection:

Advanced fraud detection algorithms analyse refund patterns and flag suspicious activity for review. Machine learning models, trained on historical refund data, identify features correlated with fraud, such as order velocity, unusual bank detail patterns, and customer behaviour.

These models generate risk scores, triggering appropriate verification intensity. High-risk refunds receive enhanced scrutiny, while low-risk requests are processed automatically. This intelligent screening approach balances efficiency with robust protection, applying scrutiny proportional to the actual risk without inconveniencing legitimate customers.

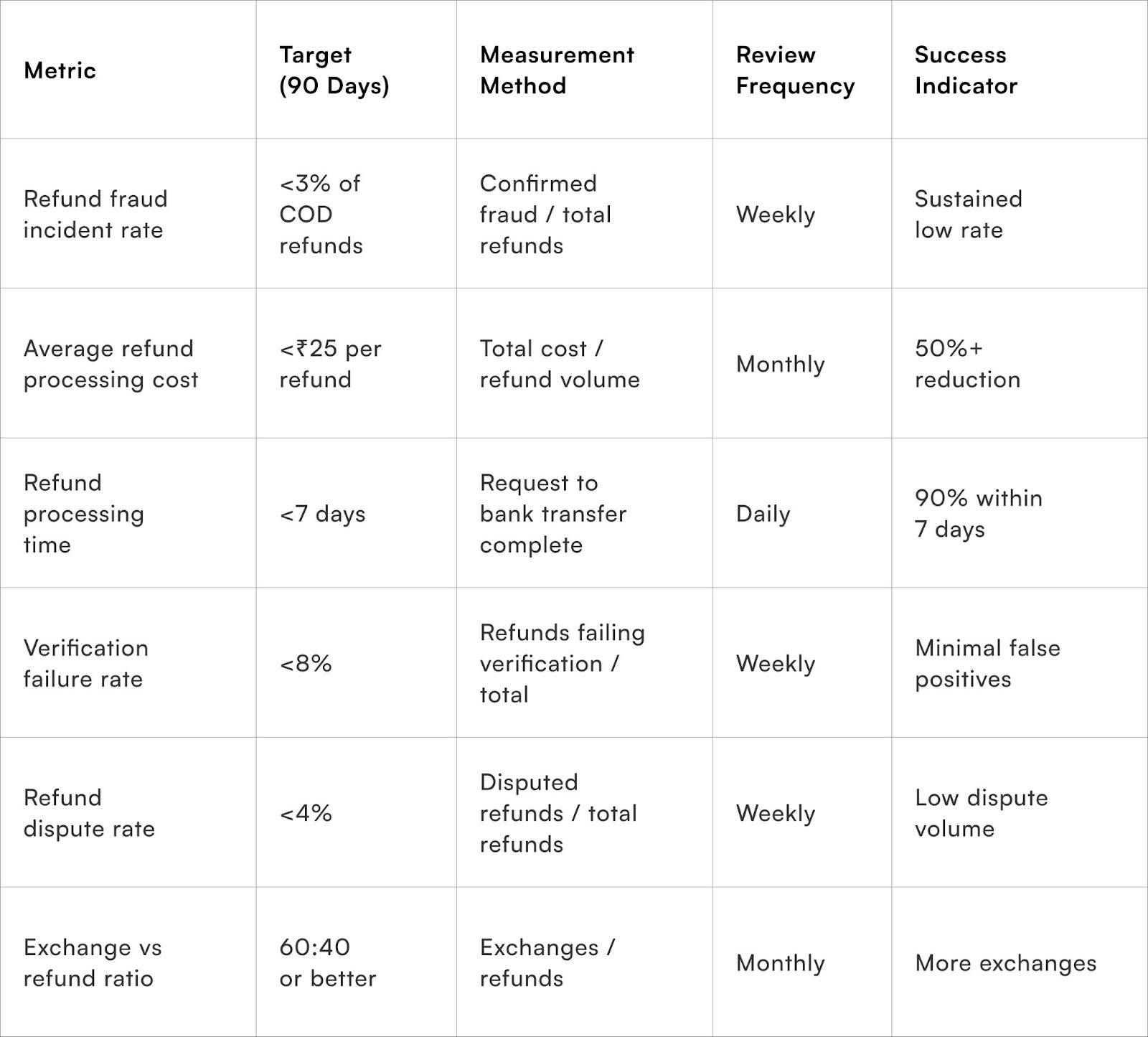

Key Metrics to Track COD Refund Risk Beyond Refund Rate

Often, brands focus narrowly on refund rate — the percentage of orders refunded vs orders placed. However, this metric alone doesn’t tell the whole story. The following KPIs offer a deeper view of COD refund risk:

1. RTO-Adjusted Refund Rate

Tracks refunds only after excluding Return-to-Origin (RTO) cases where deliveries were never completed — isolating genuine refund risk.

2. Serial Returner Ratio

Percentage of customers who have initiated multiple refunds in a defined period. A high value indicates potential fraud clusters.

3. Average Refund Value

High average refund amounts may point to targeted abuse (e.g. premium products being deliberately used and returned).

4. Refund Cycle Time

Time between return confirmation and refund completion. Longer cycles indicate operational friction that could cost customer trust and cash flow.

5. Refund Dispute Rate

Percentage of refunds that require manual review or escalation — a leading indicator of either fraud or process errors.

6. COD Reconciliation Variance

Difference between expected COD payouts (based on delivery data) and actual cash collected. Large variances can indicate leakage or reconciliation issues.

7. Refund Satisfaction Score (NPS/CSAT on refund interactions)

Operationally, a smooth refund process can still be customer-friendly even if unavoidable. Tracking this keeps customer experience in view.

Tracking these KPIs — rather than refund rate alone — allows brands to diagnose root causes and prioritise remediation instead of reacting to surface symptoms.

Quick Wins

Week 1: Current COD Refund Assessment

Analyse last 90 days of COD refunds documenting volume, refund reasons, processing times, and costs. Calculate per-refund processing cost including staff time (hours × hourly rate), transfer fees, and verification effort. Identify fraud incidents or suspicious patterns

- multiple refunds

- same bank account

- rapid order-refund cycles

- mismatched customer/account names.

Interview staff handling refunds understanding pain points and bottlenecks. Survey 20-30 customers who received COD refunds about experience clarity and satisfaction.

Expected outcome: Quantified baseline metrics showing refund volume, cost structure, fraud exposure, and specific improvement opportunities prioritised by impact.

Week 2: Policy Framework Documentation and Communication

Document current refund policies specific to COD orders with clarity on eligibility, timelines, and requirements. Revise policies incorporating risk mitigation—exchange-first language, inspection contingency, store credit options. Update checkout, order confirmation, and return request flows displaying COD refund policies transparently. Create a FAQ section addressing common questions

"How do COD refunds work?

When will I receive funds?

What information do I need?"

Train customer service team on policies and communication scripts.

Expected outcome: Clear documented policies protecting business interests whilst maintaining customer-friendly tone, with transparent communication preventing expectation gaps.

Week 3: Verification Process Implementation

Implement basic verification workflow: OTP phone verification before refund portal access, bank account name matching against order name with flagging for mismatches, delivery status checking preventing refunds for delivered orders claiming non-receipt. Create a secure refund portal form collecting bank details with validation checking IFSC codes and account number formats. Set up manual review queue for flagged cases requiring additional verification. Document evidence—order details, delivery confirmation, return inspection—for potential disputes.

Expected outcome: Systematic verification catching obvious fraud attempts whilst streamlining legitimate refund processing, reducing fraud incidents by 60-70% through basic controls.

Week 4: Automation and Process Optimisation

Integrate payment gateway payout API enabling automated bank transfers from refund portal submissions. Implement batch processing grouping daily approved refunds for consolidated transfer runs. Create a refund tracking dashboard for internal staff visibility and customer-facing status page. Set up automated communication sending customers updates at verification, processing, and completion stages. Establish weekly monitoring reviewing refund volume, processing times, verification failure rates, and fraud incidents.

Expected outcome: Reduced processing time from 15-20 minutes to 3-5 minutes per refund through automation, measurably improved customer satisfaction (65% higher NPS response rates) through transparency, and systematic monitoring enabling continuous improvement.

Measuring COD Refund Risk Management

To Wrap It Up

COD refund management requires balancing customer-friendly return policies with operational realities and fraud protection. The complexity stems from payment collection never occurring, eliminating straightforward refund pathways whilst customer expectations around compensation persist.

Successful approaches layer verification mechanisms, streamline processing through automation, and establish policies that remain generous whilst preventing exploitation. The investment in systematic refund management pays returns through reduced fraud losses, improved operational efficiency, and maintained customer trust despite necessary controls.

Audit your last 50 COD refunds identifying processing time, verification failures, and potential fraud indicators, then implement the single control that would have prevented your highest-cost problem—whether fraud, operational inefficiency, or customer dissatisfaction.

Long-term COD refund excellence requires treating this operational complexity as a strategic process deserving ongoing refinement rather than one-time policy establishment. Market dynamics shift, fraud tactics evolve, and customer expectations change, demanding regular policy review and technology updates.

Brands establishing quarterly refund process reviews, monitoring fraud patterns continuously, and testing workflow improvements achieve 23-31% additional cost reduction in year two through systematic optimisation compounding into sustainable operational advantages that refund-management-neglectful competitors cannot replicate.

For D2C brands seeking to minimise COD refund risks whilst maintaining customer-friendly policies,Pragma's refund management platform provides verification workflows, automated bank transfer processing, fraud detection algorithms, and policy enforcement tools that help brands achieve 67-73% fraud reduction whilst cutting refund processing costs by 50%+ through systematic controls balancing generosity with protection.

.gif)

FAQs (Frequently Asked Questions On The Hidden Risks of COD Refunds and How to Minimise Them)

1. Should we charge customers for COD refunds to cover processing costs?

Charging fees damages customer relationships more than it recovers costs. The ₹30-50 fee revenue doesn't offset brand damage and competitive disadvantage. Better strategy: optimise processing efficiency, reducing costs rather than passing them to customers. Reserve fees only if COD refund abuse becomes a systematic problem affecting business viability.

2. How do we verify bank account ownership without Aadhaar or PAN?

phone OTP verification combined with bank account name matching as baseline. For higher-value refunds, implement penny-drop verification—transfer ₹1, require the customer to confirm the exact amount received. This validates account accessibility without requiring government ID documents. Add a 24-48 hour waiting period deterring impulse fraud.

3. What if the customer refuses to provide bank details for COD refund?

Offer store credit as an alternative—customers uncomfortable sharing bank information can choose instant store credit instead. Document refusal and offer in communication trail. If neither option is acceptable and the customer insists on bank transfer, require additional identity verification commensurate with their security concerns justifying your due diligence.

4. Can we deny refunds for repeatedly refused COD orders?

Track refusal patterns and implement graduated responses. After 3 refusals within 180 days, restrict to prepaid-only or require manual review. Communicate policy clearly: "Multiple COD refusals detected—prepaid payment required for future orders." This balances customer access with fraud prevention, addressing systematic abuse without blanket COD removal.

5. How long should we keep customer bank account data?

Retain only for transaction completion plus dispute resolution period—typically 90-120 days post-refund. Delete or anonymize data after retention period unless customer explicitly consents to storage for future refunds. Ensure secure storage with encryption and access controls while data remains. Communicate retention policy transparently building trust.

6. How do I track the impact of C2P on refund reduction?

Use these metrics to measure C2P effectiveness:

- COD-to-Prepaid Conversion Rate: % of nudged orders that accept prepaid offer. Target: 30-50% of medium-risk orders; 40-60% of high-risk orders.

- Refund Rate by Payment Method: Compare refund % for COD orders vs. prepaid orders before/after C2P rollout.

- Expected improvement: COD refund rate stays flat or improves slightly (lost the highest-risk customers); prepaid refund rate remains low (5-10%).

- Refund Volume Reduction: Total refunds per week/month.

- Expected improvement: 20-40% reduction in overall refund volume within 2-4 weeks of C2P rollout.

- Fraud Loss per Order: Calculate (refund amount + processing cost + RTO loss) / total orders.

- Expected improvement: Fraud loss/order should drop 15-30% as high-risk COD orders shift to prepaid.

- Customer Satisfaction on Incentives: CSAT survey after C2P nudge ("Was the prepaid discount clear and attractive?").

- Target: 4/5 or higher. If <3.5/5, adjust incentive amount or messaging.

}, {"@type": "Question", "name": "How do we verify bank account ownership without Aadhaar or PAN?", "acceptedAnswer": {"@type": "Answer", "text": "phone OTP verification combined with bank account name matching as baseline. For higher-value refunds, implement penny-drop verification—transfer ₹1, require the customer to confirm the exact amount received. This validates account accessibility without requiring government ID documents. Add a 24-48 hour waiting period deterring impulse fraud."}}, {"@type": "Question", "name": "What if the customer refuses to provide bank details for COD refund?", "acceptedAnswer": {"@type": "Answer", "text": "Offer store credit as an alternative—customers uncomfortable sharing bank information can choose instant store credit instead. Document refusal and offer in communication trail. If neither option is acceptable and the customer insists on bank transfer, require additional identity verification commensurate with their security concerns justifying your due diligence."}}, {"@type": "Question", "name": "Can we deny refunds for repeatedly refused COD orders?", "acceptedAnswer": {"@type": "Answer", "text": "Track refusal patterns and implement graduated responses. After 3 refusals within 180 days, restrict to prepaid-only or require manual review. Communicate policy clearly: \"Multiple COD refusals detected—prepaid payment required for future orders.\" This balances customer access with fraud prevention, addressing systematic abuse without blanket COD removal."}}, {"@type": "Question", "name": "How long should we keep customer bank account data?", "acceptedAnswer": {"@type": "Answer", "text": "Retain only for transaction completion plus dispute resolution period—typically 90-120 days post-refund. Delete or anonymize data after retention period unless customer explicitly consents to storage for future refunds. Ensure secure storage with encryption and access controls while data remains. Communicate retention policy transparently building trust."}}]}

Talk to our experts for a customised solution that can maximise your sales funnel

Book a demo

.png)

.png)